E-commerce, or electronic commerce, has become a vital component of the global economy, and it has...

Open Banking: Transforming Financial Services with API-Driven Innovation

In today's rapidly evolving financial landscape, open banking has emerged as a transformative concept that holds the potential to revolutionize the way we interact with financial services. With the advent of open banking, innovative API-driven platforms have become instrumental in fostering collaboration, driving innovation, and enabling seamless integration within the financial ecosystem.

According to Statista, open banking is experiencing a substantial surge in global adoption, with an estimated average annual growth rate of close to 50 percent, making it one of the fastest-growing trends in the financial industry. The European market stands as the largest adopter, with approximately 12.2 million open banking users. By 2024, this figure is expected to reach an impressive 63.8 million.

Open Banking Explained

Open banking refers to the practice of securely sharing customer financial data between financial institutions and authorized third-party providers through standardized application programming interfaces (APIs). This new form of banking enables customers to grant access to their financial information to trusted third-party providers, such as fintech companies and other innovative service providers.

It is, however, important to highlight that the sharing of data can only transpire when a customer consciously opts to share their information.

APIs role in Open Banking

Evidently, APIs play a crucial role in facilitating open banking. By definition, APIs are sets of rules and protocols that allow different software applications and systems to communicate and interact with each other.

In the context of open banking, APIs act as bridges between banks and third-party providers, enabling the secure exchange of data and facilitating the access and utilization of various financial services. They also define the rules and methods through which authorized third-party providers can access and utilize customer financial data, such as account information, transaction history, and payment initiation.

More importantly, APIs ensure that the data is shared securely and in a controlled manner, thereby protecting the privacy and security of customer information.

Types of Services offered in Open Banking

Although still a nascent ecosystem compared to traditional banking, open banking offers cutting-edge solutions that are much needed in today's digital and integrated financial system. Here are some of the key services:

- Account Aggregation: Open banking allows customers to view and manage multiple bank accounts and financial products from different institutions through a single platform. This can help provide a consolidated view of their finances, including transaction history, balances, and statements.

- Payment Initiation: Open banking enables customers to initiate payments directly from their bank accounts using third-party applications. This transformative service facilitates expedited, user-friendly, and highly secure payment options, enabling seamless transactions within a retailer's website or a mobile app.

- Personal Financial Management (PFM): Open banking APIs empower developers to craft and seamlessly integrate applications that provide customers with robust financial management tools. These tools enable users to effortlessly track and analyze their spending patterns, establish budgets, and receive tailored recommendations for optimizing savings and exploring lucrative investment prospects.

- Loan and Credit Services: Through open banking, lenders can access a customer's financial data, including transaction history and income, enabling them to make more precise lending decisions. This also empowers customers to effortlessly compare loan and credit options from various providers based on their unique financial profile.

- Identity Verification: Open banking APIs can be utilized to verify a customer's identity and financial information with greater efficiency. This, in turn, reduces the necessity for manual documentation and enhances the overall user experience, enabling secure and seamless customer onboarding processes.

Open Banking Vs Traditional Banking

Data Sharing

Open banking is characterized by the sharing of customer data between different financial institutions and authorized third-party providers (TPPs). It allows customers to give consent for their financial data to be securely shared, facilitating enhanced financial services. In contrast, traditional banking typically keeps customer data within the bank and limits access to external parties.

Innovation and Competition

Open Banking promotes competition and innovation in the banking industry by encouraging the development of new financial products and services. With access to customer data, third-party providers can create innovative applications and solutions that cater to specific needs. Traditional banking, on the other hand, is more centralized and controlled by a limited number of banks, which may hinder rapid innovation and competitive offerings.

Customer Control and Personalization

Open banking emphasizes customer control over their financial data. Customers can choose which data to share and with whom, empowering them to find better deals, personalized services, and more tailored financial advice. Meanwhile, traditional banking offers limited control to customers over their data, and personalized services may be restricted to the products and services offered by their bank.

Regulatory Framework

Open Banking is typically supported by a regulatory framework that governs the sharing of customer data and the operations of third-party providers. Governments and regulatory bodies play a role in ensuring data privacy, security, and transparency in the open banking ecosystem. While traditional banking also operates within a regulatory framework, the regulations may differ in scope and focus, with the latter often prioritizing the stability and integrity of individual banks rather than promoting data sharing and competition.

Is Open Banking safe?

While open banking brings great potential, it also introduces certain challenges that must be addressed. Data security and privacy are of utmost importance in open banking ecosystems, necessitating the implementation of robust security measures, encryption standards, and secure authentication protocols to safeguard customer information.

Fortunately specific regulations have been put in place to enhance the security of open banking services. In Europe, third-party providers are required to be registered with a national regulatory agency, ensuring that only authorized entities can access your bank account information with your explicit consent. Moreover, these providers must demonstrate compliance with security and fraud prevention procedures and adhere to minimum service level agreements, ensuring the protection of your data.

Additionally, the introduction of common standards is playing a significant role in shaping the creation, sharing, and access of individuals' data. National bodies and regulators, such as the Financial Data Exchange (FDX) in the United States, are keen on these standards. The FDX brings together banks, fintech companies, and financial services groups to establish a unified data-sharing standard, which has the potential to accelerate the adoption of open-banking API frameworks on a global scale.

To further enhance security measures, the open banking industry is embracing the concept of "tokenized" access, commonly referred to as "Open Authorization" or "oAuth" connections. In this system, a third-party entity is granted a unique "token" instead of direct access to your bank account credentials. The token acts as a secure substitute, ensuring that even if it is compromised, it carries no significant value, thus providing an additional layer of protection for your sensitive information.

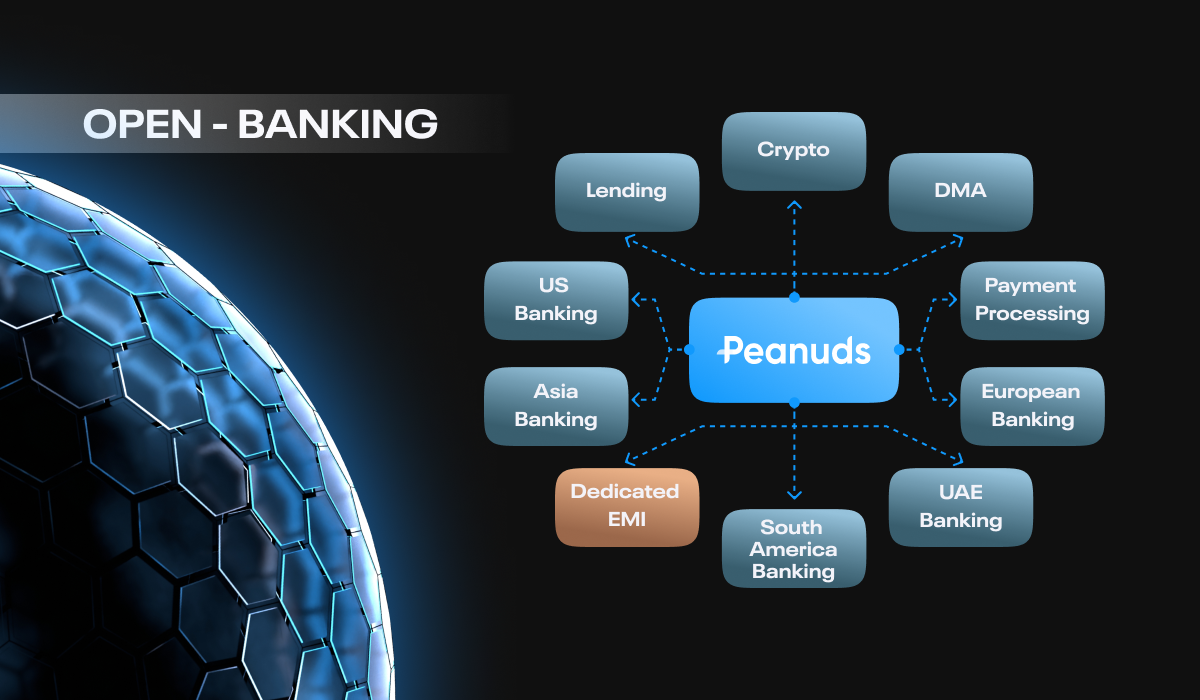

Peanuds: A Modern-Day Payments Solution

Amidst the transformative wave of open banking, Peanuds emerges as a modern-day payment solution that empowers individuals and businesses with seamless connections to specified fintechs or EMIs (Electronic Money Institutions) and BaaS (Banking as a Service) Providers.

By leveraging the power of open APIs, Peanuds facilitates an integrated finance experience, enabling customers to access a diverse range of financial services and products through a single platform.

With Peanuds, users will be able to effortlessly manage their finances, explore innovative solutions, and unlock the potential of open banking.